made

for a happy day

How should I invest my money in 2009 | 2010?

Most Brits must have wondered how to get a return on their savings in

2008. Many will have watched in dismay as banks went wobbly, share portfolios

were clobbered and interest paid on their savings accounts ran dry.

Could we have invested better over the last few years?

Since 2006, gains could have been made by:

1) Selling a house rather than buying in 2006|7

(Graph

shows average UK house prices since 1975)

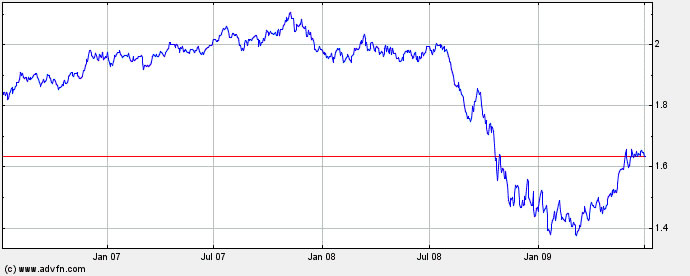

2) Swapping pounds for dollars then swapping back later

(Graph shows how many dollars a

pound bought over 3 years)

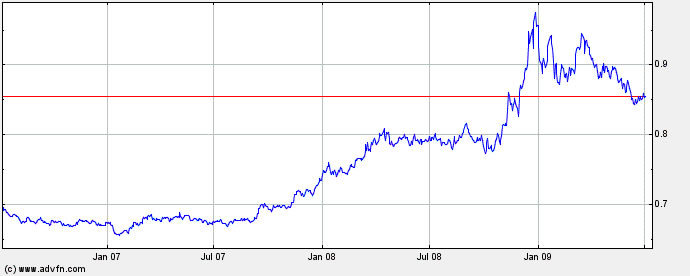

3) Swapping pounds for euros then swapping back later

(Graph shows how many pounds a euro

bought over 3 years)

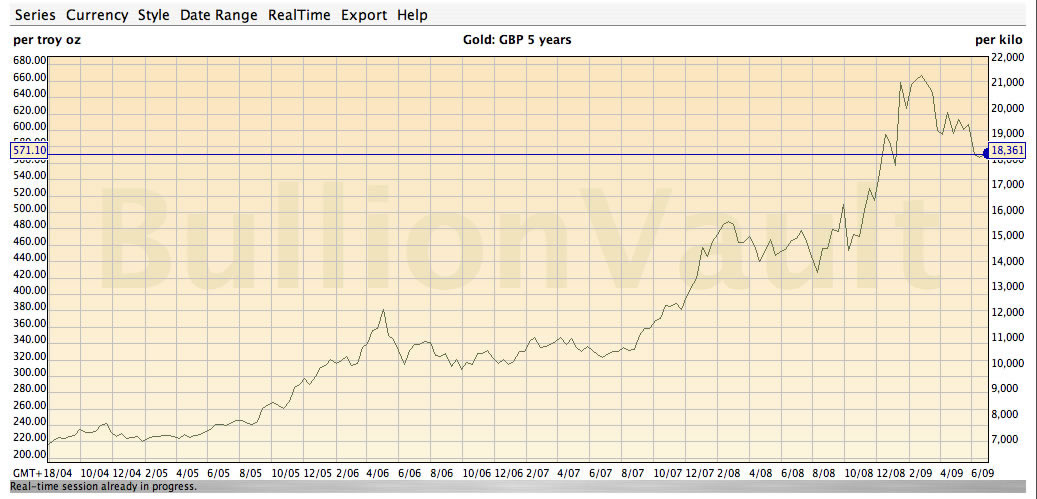

4) Buying gold coins in 2006 and selling earlier this year

(Graph shows value of one ounce

of gold in pounds over 5 years)

I suspect few of us went for this.

So, how could we invest better in 2009 and 2010?

First things first.

If today's financial crisis teaches us anything, it is that the mass media

won't help us invest wisely. Taking tips off the TV is like popping pills

only to later discover the full horror of the potential side effects.

In fact, when media pundits tell us that everyone else is piling into

a particular investment (like buy to let properties, or dot.com shares)

history often suggests its a very good time to be doing the exact opposite.

My advice to myself for 2009|10 is.... RELAX:

1) Don't be fooled into thinking the downturn is over. House prices and

shares are set to fall further. *1

2) Hold your cash in a safe place where you can access it immediately.

*2

{kind=link}

{kind=link}

{kind=link}

3) Clear existing debts and avoid taking on others. *3

4) Avoid buying bonds (ie. government, bank or company IOUs) until a realistic

rate of interest is being offered on the latest issue.

5) Do some social lending somewhere like Zopa.

As reliable borrowers look to clear high interest credit card debt, your

offers of a tenner here and there at 10% interest will look attractive.

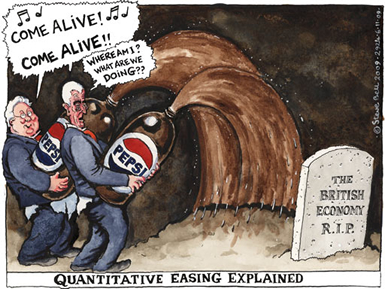

In particular, bear in mind that we are currently in a special period.

Downward trends have been temporarily arrested by something called quantitative

easing. This is the process by which central banks in the UK and US

are creating money. This is being used to prop up all sorts of investments

for which demand has dried up. This has arrested the crash but is not

a credible long term tactic.*4

Ends | 4 July 2009 | The Leg

comment | back to top | thoughts

-

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

- - - - -

Notes:

*1 Don't even go there until you see repossessions approaching 75,000 over the last 12 months or the FTSE 100 nosing below 2500 points. Rising unemployment doesn't create demand for mortgages, goods and services.

*2 Savings account interest rates are liable

to rise steeply in 2010. You won't want your savings committed to a long

term bond promising low rates of return at that point.

*3 Servicing debt is going to get more and

more expensive as banks are forced to get themselves on a more stable

footing.

*4 Continued forced inflation of the money supply could result in a currency crisis. Interest rates would have to be hiked to keep investors in sterling. It is not beyond the realms of possibility that this could be the first serious difficulty to face a new government after elections in 2010.

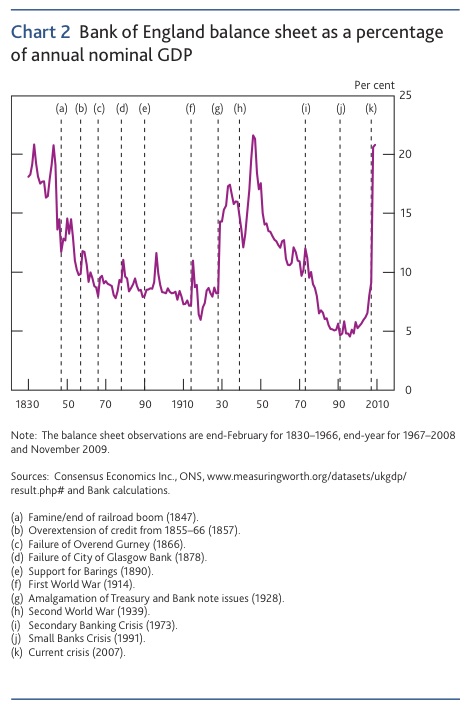

Essential Reading:

Reflections on the Great Depression

of 2010

See GRAPH for % of GDP driven

by gov. stimulus, now and b4

{kind=link}

Related Articles:

2013:

23 Jun: BIS warns

banks to plan their exit from QE strategies

8

Apr: BlackRock urges Fed to half its $85bn/mth QE3

4

Jan: Gold heads for longest run of weekly losses since 2004

2012:

9 Dec: Latest BIS

Report - asset

prices propped up by QE

24

Oct: Mervyn King - stimulus "cannot continue indefinitely"

11

Jul: When we finally cut our debt the impact will be massive

28

Jun: GDP data confirms UK now in double-dip recession

24

Jun: Oh Dear - BIS warns that QE puts UK's credilitity at risk

15

Jun: £140bn more loose loans to banks refeeds speculation

6

Jun: Foreign rich inflate central London prices whilst rest fall

23

May: Who is buying government bonds? The ECB

2011:

6

Oct: BoE Head launches further £75bn in quantitative easing

3

Aug: Lenders run to hold cash rather than lend to each other

3

July: Collateral demand rises for interbank lending

26

June: BIS foresees demand destruction & rising rates?

11

June: IMF - QE

& low interest rates mask vulnerabilities (p4)

2010:

5

Sep: "The US has run out of bullets" says Nouriel Roubini

9

July: Fund managers move into cash (up to 40% of portfolio)

7

May: Pound falls to $1.47 following UK election results

27

Apr: Yield on traded Greek 2 year bonds surges to 17%

26

Mar: Yield on traded US 10 year treasuries rises to 3.92%

16

Mar: UK home reposessions rose to 54k in 2009

13

Mar: Credit card limits now being slashed

1

Mar: Pound dives 4 cents to $1.47 in two hours of trading

28

Feb: Yield/interest on traded UK 10 year gilts rises to 4%

16

Feb: UK credit card interest rates at highest for 12 years

4

Feb: Quantitative easing suspended? (started Mar 09)

1

Feb: Rate on bank personal loan rises to 9% on 3yr loan

2009:

29

Dec: FTSE100 returned to pre-Lehman collapse level

25

Dec: Problem for Housing in 2010? Rising Interest Rates

22

Dec: UK economy still contracting (0.2% in Q3)

11 Dec: 10 Year bond's price falls at Darlings pre-budget report

6

Dec: Distrust in banks leads people to hoard cash

24

Nov: BoE propped up RBS/HBOS with secret £61bn loans

23 Oct: The emergency measures propping up the UK economy

6

Oct: Global markets rally is 'too much, too fast'

4

Oct: HSBC Chief fears a second downturn

10

Sep: Co-operative (mutual) Bank's profits up by 11%

23 Aug: The risk of a double-dip recession is rising

12

Aug: Strategist prepares clients for FTSE 100 falling to 2500

10

July: Cash is king for investors

7 July: BoE just ploughed £107bn into UK government bonds!

29

June: CBI survey reveals bad debts growing fast